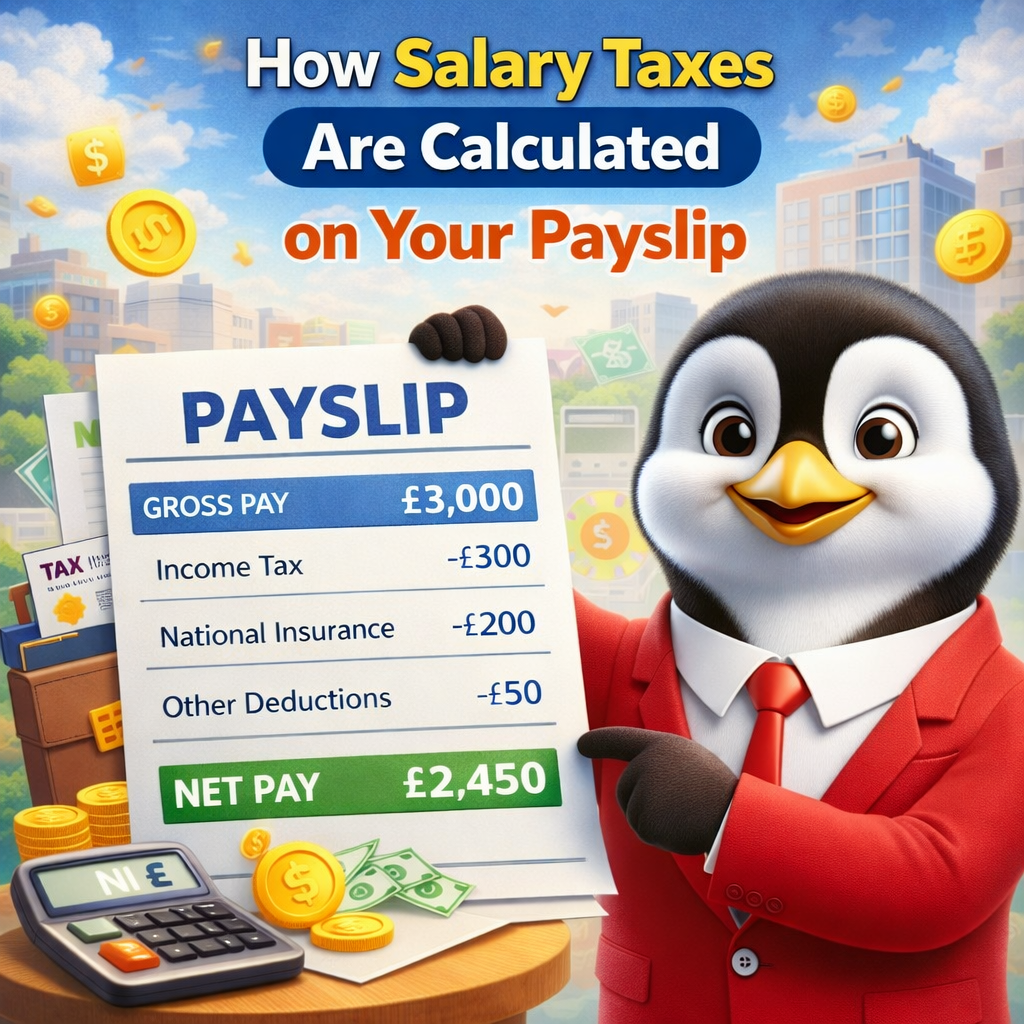

Your pay slip can look like a mini puzzle. You see gross salary at the top, then several deductions, and finally a net pay number that lands in your bank account. If you’ve ever wondered why the “final” number feels lower than expected, you’re not alone.

The good news is that pay slip taxes usually follow a clear pattern. Once you understand the moving parts, the deductions start to make sense. Better still, you can predict changes before they surprise you—especially if you run a quick estimate with a salary tax calculator.

Let’s break down what’s happening on a typical pay slip and how the math is usually done.

Start with gross pay

Everything begins with gross pay, which is your earnings before anything is removed.

Gross pay might include:

From there, your pay is adjusted through deductions. Some deductions reduce taxable income first, while others are applied after.

Pre-tax vs post-tax deductions

Not all deductions work the same way. This is where many people get confused.

Pre-tax deductions

These are amounts taken out before income tax is calculated (depending on your country and plan rules). Because of that, your taxable income can be reduced.

Examples often include:

-

Retirement contributions (some types)

-

Health insurance premiums (in many payroll setups)

-

Specific benefit programs supported by local regulations

Post-tax deductions

These are taken out after taxes are calculated. They don’t reduce taxable income, so they mainly reduce your final take-home pay.

Examples may include:

-

After-tax insurance add-ons

-

Loan repayments through payroll

-

Garnishments (where applicable)

-

Voluntary contributions or memberships

As a result, two people with the same gross pay can have different net pay if their deductions differ.

Withholding is an estimate, not always the final tax

On most pay slips, the tax line is not your “final yearly tax bill.” Instead, it’s withholding—an estimated amount collected each pay period.

That estimate is based on things like:

-

Your income level

-

Your declared filing status (where applicable)

-

Your allowances, exemptions, or credits (depending on local rules)

-

Payroll tables or tax rates used for that period

Because withholding is an estimate, it can sometimes be slightly high or low across the year. Then, your final tax is settled during tax filing (if filing applies in your country).

This is also why a salary tax calculator can be helpful: it gives a practical “what will I take home?” picture without requiring you to decode payroll tables.

Common tax lines you’ll see on a pay slip

Your pay slip deductions may vary by country, but these categories are common globally:

1) Income tax

This is the main tax on earnings. In many systems, income tax is progressive, meaning different portions of income can be taxed at different rates.

2) Social contributions

Many countries collect mandatory contributions for social programs (such as pension, healthcare, unemployment insurance, or similar). These can appear as separate line items.

3) State/province/city taxes (where applicable)

In some places, local taxes apply depending on where you work or live. Therefore, location can change your deductions even with the same salary.

4) Employer benefits

Some benefits are split between employer and employee. So, you might see your portion listed as a deduction.

Why your net pay changes even when your salary doesn’t

This is a big one—and it’s more common than people expect.

Your take-home pay can change because:

-

You changed benefit plans (health, retirement, etc.)

-

A bonus was added (with different withholding rules in some systems)

-

Your tax code / withholding settings were updated

-

You crossed a threshold (certain contributions may cap or shift)

-

You worked different hours or had unpaid leave

So, if your net pay suddenly drops or rises, it doesn’t always mean something is wrong. Instead, a payroll factor usually changed.

The simple pay slip formula you can remember

To keep it practical, think of your pay slip like this:

Gross pay

→ minus pre-tax deductions (if any)

→ equals taxable pay (often)

→ minus income tax withholding

→ minus social contributions

→ minus local taxes (if applicable)

→ minus post-tax deductions

= net pay

This helps you spot what’s driving the difference. It also helps you ask better questions if something looks off.

Where calculators fit into real-life planning

Most people don’t want to manually calculate each deduction—especially when comparing options.

A calculator is useful when you’re:

-

Evaluating a new job offer

-

Negotiating a raise

-

Planning how a bonus might impact take-home pay

-

Adjusting benefits and wanting to see the net change

-

Budgeting monthly expenses accurately

In these moments, a salary tax calculator gives you a quick estimate so you can plan confidently. And if you want to isolate deductions and understand what’s reducing net pay, a tax deduction calculator style breakdown can be especially helpful.

Quick tips to read your pay slip with confidence

-

Compare gross pay to taxable pay (if shown) to see what benefits reduced tax.

-

Scan the deduction section first—most changes show up there.

-

Check whether any deduction is one-time (bonus month, annual fee, correction).

-

Keep an eye on filing/withholding settings if your system uses them.

-

Save one pay slip per quarter so trends are easy to spot.

Small habits make pay slips feel far less confusing.

Use HRTailor.AI Income Tax Calculator

If you want a faster way to estimate take-home pay and understand pay slip deductions, Try HRTailor.AI – Income Tax Calculator. It helps you model salary scenarios clearly, so deductions feel predictable not confusing. Many people also use a salary tax calculator approach here to compare offers, raises, and benefit changes without guesswork.